Don't get stopped out - a different view of risk management

All entities from individuals to governments should manage risk the same way. The most important aspect of risk is not volatility

SUMMARY

In this note, I share a slightly different approach to risk management, which potentially leads to different conclusions about investment management and financial planning. 1

Individuals, corporations and even governments can take the same approach to effective financial risk management2.

Volatility is a popular, but poor metric, and rarely can it be used to make good investment decisions, although it is often described as a foundational risk metric (some have called it a currency) and used to sell financial products.

And finally, all financial assets and liabilities are exchanges of money now, for money later. Any time one cannot describe or think about a financial asset this way , it is worthy to consider what else the asset is really like.

WHAT IS FINANCIAL RISK AND HOW IS IT MEASURED

The dictionary definition of risk is “exposure to danger.” I believe that all financial risks are rooted in what an entity owes or wants to spend and the danger is an inability to spend or pay what one owes. It is important not to minimize that financial risks, for many people, can extend beyond 1s and 0s and present non financial danger.

Going forward, I’ll call what an entity owes a liability and and what it wants to spend a goal. Whether we like it or not, financial resources are required to achieve our goals and resolve our liabilities. These resources come from either income earned or through the liquidation of assets previously purchased or gifted to us.

An interesting way to think about this is to imagine that you do not have any liabilities or goals at all. Imagine that you do have a lot of assets and plentiful income. In this scenario, I am positing that you actually have no first order financial risks. That is to say, you are impartial to what happens to the value or quality of assets or money. There is neither danger, nor any benefit to be gained if they are doubled or halved and if you believe what I am saying, it also means that wealth is philosophically and practically unique to an entity. This topic is a rabbit hole for another day.

Additionally, most non professional investors believe that the largest risk involves the potential for the value of an asset to go down. This is directionally right, but an incomplete conception for many reasons, to mention a couple:

New liabilities and goals can change instantaneously, rendering stable assets insufficient - ( new goals, obligations or inflation)

Many risk measures focus on price, rather than value. The price of things are (usually) the same for everyone, whereas the value is generally not.3

I remember when I was responsible for a small part of the “Bad Bank” at my former employer UBS and one earnings period the CEO announced that Return on Equity Targets (ROE) would shift from 12.5% to 14.5%. For most people this is sort of innocuous and forward looking, but for me this was a disaster, an event just as risky as an unexpected Fed hike causing a fixed rate bond portfolio to fall in value. some trades that made sense yesterday were suddenly underwater, and rather than an exogenous event causing us to underperform, a new goal (and new expectations created with our investors) instantly made our assets insufficient.

A more cogent way to define "risks" is "an event that degrades one's ability to fulfill their liabilities". The causes of these events are either internal or external to the entity. A few events probably end up driving the majority of the value creation or destruction to an entity, so risk management involves considering these events for as far out in time as is practical.

Taking it a step further, to manage risk, one could build a financial model which is just a function, or group of functions, which identify the major variables which can affect the price of assets. Then you collect evidence about how predictive these functions are at determining future cashflow - this cashflow can be from a sale, or from distributions. These models can help an entity survive all the risk events it can imagine and prepare for the inevitable ones which it cannot predict.

NO ENTITY REQUIRES SPECIAL FINANCIAL RISK MANAGEMENT

The intensity of risk management in an entity is mainly driven by

the personality of the controllers in an entity,

what is at stake and

their resources.

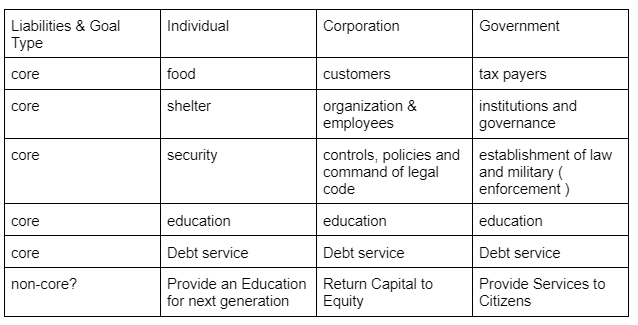

Beyond that, all entities have core and non core liabilities and goals. Below is a very rough comparison of core and non-core goals and liabilities for different types of entities:

Any entity which fails to cover their core needs in the short term will fold or try to borrow money. This can be borrowing for fixed payments (debt) or borrowing in exchange for the promise of a proportion of free cashflow, (equity). Those who cannot deliver on the promises outlined in these agreements will either have to use some power to defend themselves, or be wiped out, at least financially.

All these entities have the following:

Expenses that are hard to associate with future income ( eg. spending on education)

Expenses that are easy to associate with future income ( eg. financial assets )

Income that clearly services these expenses

Income that is in excess and not associated with a known expense today (so must be invested)

Methods to raise capital when income cannot cover current expenses

Methods to invest excess savings when income surpasses current expenses

A process that attempts to understand the interactions between income and expenses now vs later.

Individuals have to find a way to pay for food and shelter, and maintain a minimum level of education and security, or be dominated by other entities' self interest. Those who do this well and who benefit from good fortune, have excess funds which can be invested in corporations, fiat money, precious metals or commodities.

Corporations need to establish policies and a culture, invest in a way that finds and maintains paying customers and engage with the government in control in order to return capital to the individuals above, based on some contract (or a raw power dynamic)

Governments need to find a way to placate tax payers by providing them with services, defend their currencies, borders and rules, in some cases investing in policies which will finance future expenses.

In the end, the fundamental goal for all entities is to not get stopped out, and while the tools may be different the approach is the same in the long run.

VOLATILITY IS NOT A RISK METRIC

I know this is not quite true but volatility comes in so many different shapes and sizes, and I’m only going to list 2 because I’m by no means an expert:

Measured Volatility - the standard deviation of price from a selection of data points (for example all the prices while the market is open)

Implied Volatility - within a mathematical model, the input standard deviation of price required to return the price of a traded security

Measured volatility tells us about how past events have influenced prices and implied volatility tells us the markets best guess of how future events will influence prices, but neither tells us about what factors make prices move up or down. If prices are the discounted value of future cash flows, then once we know the discount rate and the mean/expected future cash flows, volatility just tells us how much these things have (or are expected to have) collectively deviated around the mean.

Further, all volatility is not created equally - one can compare an asset that transacts 1 million times in 1 year, with one that transacts 100 times in on year. Maybe there are some math approaches to resolving this, but generally comparing the volatility of private real estate, to that of liquid REITS for example is wrong. Clifford Assness has called this #volatilitylaundering, the idea that volatility and safety are related makes many people try to express whatever they are doing as less volatile.

Even worse, we have been convinced that if there are no prices at all, that an asset is less volatile. When in fact, no prices means that the asset is more volatile. If tomorrow AAPL had no buyers for 1 hour, only PE managers would celebrate this as a feature and not a bug!

A company who is consistently able to produce more income than expenses over time, can largely ignore the “risk” of equity price volatility. When raising capital is necessary for survival, this is a completely different story.

FINANCIAL ASSETS ARE EXCHANGES OF MONEY NOW FOR MONEY LATER

It is an unavoidable truth - whether the money later comes in the form of distributions, or as a result of a sale, all assets are just exchanges of money now for money later. As discussed above, risk is introduced when the future cashflows are not certain.

Michael J. Mauboussin recently wrote about this in depth, - for investors - the only thing that should matter is where the future cashflows will come from and how to discount them. This is very very different from the activity of a trader, who is less concerned about value and more concerned about extracting money from price movements.

To be more precise, we have to define what money is - anything with buying power. With this in mind, just as one entity's income is another entity's expense, it is also true that one entity's financial asset is another entity's financial liability.

Very simplistically, discount rates enable us to compare money now to money later and are the glue that helps us manage financial risk. We generally have to make bets about two things at a high level:

how much money will be available later (in exchange for selling our asset or via distributions from our asset)

What rate should I discount it? Or said a different way, how much more worth it is it, for me to have this buying power today.

Since we know with certainty that we will be wrong about the amount of money and rates (how much we could earn if we had this buying power today) good financial risk metrics are inputs in a function which we can use repeatedly to guess the future value, and generally we should care more about the sensitivity of each of these inputs.

Clarifying goals and core needs by first translating them into cash flows, means that they can be compared more easily to financial assets. Then organizing, analyzing and creating strategies to service these cash needs over time ensures that real assets are greater than real liabilities over time.

This does not mean that entities with negative cashflow today are necessarily less valuable, it just means that the further out and less clear the source of positive cash, the larger the risk.

Very recently, the ripple effect of the FTX default has reminded a lot of people that despite the novelty of web3 and the similarities to money and currencies, you cannot violate this rule about money now and money later.

When I say traditional risk management, I mean market risk, which generally is born out of modern portfolio theory and the approach of creating a portfolio that maximizes return for a level of risk - risk in this approach is defined as the volatility of asset prices.

Financial risk management is the process of identifying, measuring and controlling parameters which expose the value of an asset to change. When implemented this can mean allowing for a lot or little change based on an entity’s goals.

I’ll write something about price and value shortly