Lenders of First Resort

A new BIS study highlights the risks within the biggest financing market on the planet

On an average day in 2022, foreign investors borrowed about $85 trillion using foreign exchange (FX) swaps, an amount sufficient to buy roughly 22% of all US assets. To put this in perspective:

The total value of privately held US Federal debt is $171 trillion.

And the repurchase agreement or repo market - the largest securities financing market on the planet, results in $3 trillion per day in loans.

The total value of us mortgage backed securities is $12 trillion

The repo market is a frequent subject of inquiry into the fragility of US monetary policy implementation. In the current “excess reserves” regime,2 where quantitative easing and tightening are the main drivers of policy transmission, the stability and cost of financing US Treasuries is as important as ever.

The Bank for International Settlements is, however, concerned about the FX swap market because of its sheer size and lack of accounting transparency: FX swap transactions are reported on balance sheets as derivatives, despite having very non derivative economic characteristics. There may be some merit to this concern, because there are good arguments for why FX swaps probably have a greater impact on financial conditions than most levers within the Fed’s control.

What is an FX swap anyway?

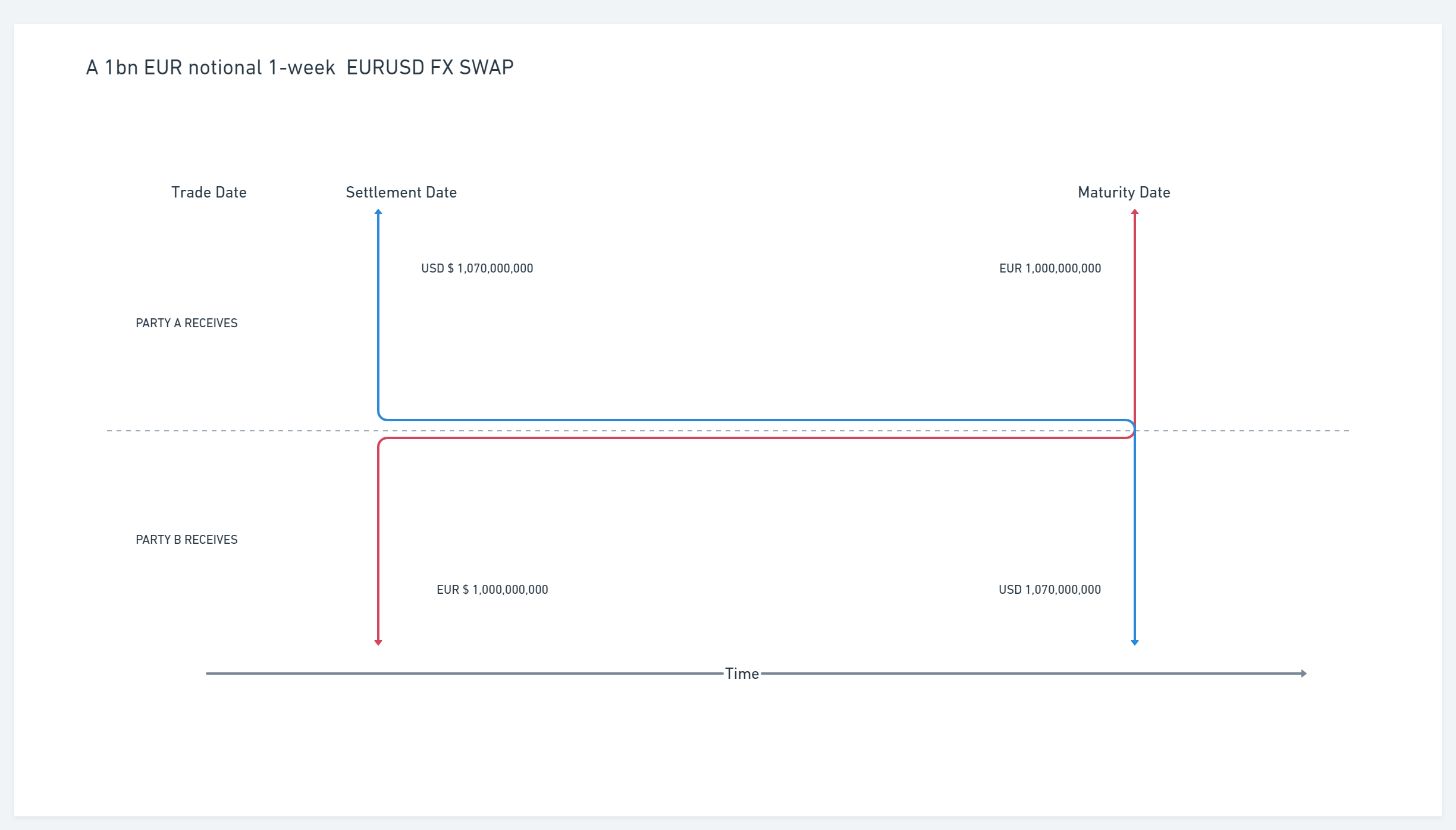

A Foreign Exchange (FX) swap is a derivative contract in which an entity loans a currency to another entity (commonly called a “counterparty”) and, at the same time, borrows another currency from the counterparty for a preset period of time. These transactions are generally executed over the counter (or not on an exchange), and they are different from the vast majority of derivatives in one important way: The buyer and the seller must actually exchange the principal amount referenced in the derivative contract at the beginning and end of the transaction.

Most derivatives, by contrast, are designed to produce a net payment which mimics the performance of having owned the referenced or “underlying” security - hence their names, however the entire profit or loss from FX swaps is a result of 4 large payments.

This differentiates FX derivatives from most of their equity, commodity or interest rate cousins because the capital at risk and the requirements to perform are much more substantial.3 If you enter into a 1bn dollar total return swap on AAPL , or a 1bn dollar 10 year USD interest rate swap, one only has to exchange collateral equaling the daily mark-to-market of the transactions alongside some amount of initial margin in the 10s of millions. Interim payments of interest vs the underlying performance are equally small compared to the face value or “notional” of the swap.

If you enter into a 1bn dollar EURUSD FX swap, you need to find 930 million euros in two days time and the other party needs to find 1 billion dollars. Suffice it to say it just hits different.

Why do FX swaps exist?

Real assets are not distributed equally along country lines, and assets produced by resourceful individuals and corporations follow suit. Often, people with money somewhere want to buy real and financial assets somewhere else and they generally have three options:

Buy the currency which the asset is denominated

Borrow the currency which the asset is denominated

Earn income and save up in the currency which the asset is denominated

You can skip this section altogether if you’re familiar with the above concept, but one way or another, unless you have earned US dollar income or were “born” with it, (i.e you are a US bank) you cant buy AAPL or US government bonds as a foreigner without first buying US dollars.

This is a simple but fundamental point. As the US has grown to be the largest economy - savings across the globe have made their way to dollar assets. As the current reserve currency, crucial goods like oil settle in dollars and many countries issue debt denominated in US dollars to attract investors who want their savings in the currency that everyone else wants.

Every time that a real assets is leveraged, a financial asset is created, alongside a mirror image financial liability

Most assets in the world are leveraged, raising cash for their owners. The largest example of this is real estate, which is 2/3rd of global real assets.4 Real assets are defined as land, natural resources, buildings, infrastructure, machinery, equipment, precious metals and intellectual property or intangible assets. Every time a real assets is leveraged, a financial asset is created, alongside a mirror image financial liability for the borrower.

Taking the simple example in real estate:

You want to buy a home for $300,000

You do not have the good fortune of having saved $300,000.

But you do earn about $100,000 a year and have saved $150,000.

A bank will lend you $225,000 to buy the home

You buy the home and you have $75,000 left over to furnish it, alongside keeping a little rainy day fund.

You become a small part of a financial asset which is then sold to investors, local and foreign

This is a boring example because it is standard practice and this type of credit provision allows for all sorts of good things. Things gets more interesting when you go beyond an individual buying a home and consider an institution buying a similar real asset. Let us say that you are a Swiss pharmaceutical company like Roche and you would like to buy a $300mm distribution facility in the USA. You have a couple different options

Buy it with local currency savings - Take 280mm euros of the companies cash and buy 300mm dollars, you use the $300mm to buy the facility

Get a foreign (dollar) commercial loan- Enter an agreement with a US bank to borrow 225mm dollars. Take ~70mm euros and buy 75mm dollars, then use the $300mm dollars in total to purchase the facility

Buy it with USD savings5 - Take some of the US dollar earnings from sales of drugs to Americans in the amount of 300mm and use it to buy the facility

Use an FX swap Enter an agreement with a bank to borrow $300mm for 3 months, In exchange lend them 280mm euros for 3 months, use the $300mm to buy the facility6

So why could this be a problem?

One peculiarity of the FX swap market is the distribution of maturity. 80% of FX swaps are less than 1 month long, 70% are less than 1 week long and 30% are only executed overnight.

One way to think about this is that for the past 20 years financial institutions call each other, every single day, to borrow ~ $25 trillion dollars. So inevitably, bad things feel like they are about to happen (risk off events) and or on crucial event dates like month ends, quarter ends and central bank meeting dates, the US banks who normally have surplus dollars, no longer do. As a result it is fairly common for the supply of dollars to get squeezed multiple times a year.

It is not uncommon for those blessed with USD on these days, called “turns” to charge eye-watering rates. When I was trading, it was not uncommon for market participants to pay implied rates of upwards of 25%, to borrow dollars against certain currencies on some of these days. Keep in mind this is 25% for a few days of a loan collateralized by another G10 currency, so this is a really high number.7

In the early days of the pandemic, similar fears which took hold during the global financial crisis in 2008 were revived. Institutions which depend on these swaps had a two fold problem:

First, for ever unit of dollar debt at non-financial institutions domiciled outside of the US, there are about 2 additional dollars of FX swaps used to pay for things these companies owe in dollars and/or buy financial and real assets. These assets tend to have a maturity greater than 1 month, creating a consistent maturity mismatch.

Second, there tends to be a correlation between asset prices dropping, and reductions in collateralized lending capacity.

For foreign owners of US assets, if your bank does not roll over your loan, your only options are to sell those assets to cover loans or outright buy dollars to fulfill your obligations(see above). Generally, stressed borrowers choose the first option kicking of a cycle:

selling of USD assets…

causing others with better credit quality to watch prices suffer and consider selling their positions for risk reasons and not credit reasons…

further putting pressure on other borrowers who’s collateral is losing value…

causing banks to pull back USD lending

This sort of cycle was a core part of the process which created chaos during all of the global financial crises. In 2008 for example, European banks used method # 2 (commercial paper) and method # 4 (FX swaps) to pay for almost $8 trillion of US dollar assets. Once they lost access to these lending markets, they had no dollars left to deal with the collateral calls or pay back their rolling USD loans. Their only choice was to start selling euros and eventually to sell the assets they held - mainly US mortgage backed securities.

Fast forward to today and this figure is now $36 trillion for non us banks and $24 trillion for non financial institutions. The concern today is that either a pullback in liquidity or repricing of assets could trigger a new cycle across a broader set of asset classes. A 10% reduction in liquidity in fx swap markets, for more than 7 days, would affect the financing of 8.5 trillion dollars of real and financial assets - comparing this to any single sector of the global balance sheet, this is a big number.

A reduction of availability or disruption in FX swap markets would have a significant impact on all asset classes in a way that most US investors probably don’t consider. It is a low probability, but very high impact event which would be more impactful than an unexpected change in the Fed funds rate or the path of QE. It is probably worth most investors considering how they would navigate this scenario should central banks not be able to step in fast enough. The BIS is asking the central banks and regulators to be prepared.

Thanks to Andrew Hansen for thanks reading this post in draft.

If you made it this far, you probably own more things than stocks and bonds and you’ve earned a shameless plug for my real job

If you are looking for the simplest way to organize and invest in private and alternative assets - join the waitlist for Distributary!

https://www.dallasfed.org/research/econdata/govdebt#charts

https://www.federalreserve.gov/econres/notes/feds-notes/implementing-monetary-policy-in-an-ample-reserves-regime-the-basics-note-1-of-3-20200701.html

Every analyst who joins a macro derivatives desk will probably have heard some story of a young trader who was delivered a truckload of pork belly futures because they failed to close out a futures contract - but this type of situation is an error and not by design.

Real assets are defined as https://www.mckinsey.com/~/media/mckinsey/industries/financial%20services/our%20insights/the%20rise%20and%20rise%20of%20the%20global%20balance%20sheet%20how%20productively%20are%20we%20using%20our%20wealth/mgi-the-rise-and-rise-of-the-global-balance-sheet-full-report-vf.pdf

This option is tricky. Roche Investors gave Roche CHF in equity and they want CHF back. Roche’s treasurer probably sits around each year and says - should I sit on a big pile of USD from all of my USD sales? The investors who need to sell Roche shares to buy ski chalet’s probably would like to manage this excess currency risk themselves.

This seems crazy right? buy a fixed asset using a 3 month loan! This is fairly common and there are realities about the availability of financing and the term structure of interest rates that has made this much more common than most people imagine.

Its important to note that the volume of transactions which pay these rates are generally low. Generally, financial institutions build entire systems to ensure that they are not short dollars over these periods and it is the non financial participants who have no choice but to borrow the dollars required to meet their liabilities. These are in the hand full of billions, a trivial amount in the context of the overnight fx swap market